As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

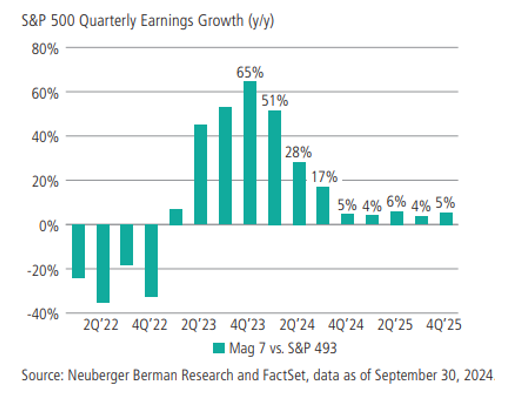

We believe we are on the cusp of a new economic cycle. In fact, Goldman Sachs is forecasting S&P 500 earnings to accelerate from 9% in 2024 to 15% in 2025. Importantly, the annualized earnings growth differential between the Mag 7 and the other 493 stocks in the S&P 500 Index is expected to shrink from a peak of about 65% in 4Q 2023 to about 15 % in late 2024. We believe this gap will continue to diminish in 2025 as earnings growth begins to broaden out to other economically sensitive sectors like financials, industrials, and materials.

Currently, the weight of the largest 10 stocks in the S&P 500 is about 37%, which is in the 97th percentile since 1964 and well above the Tech Bubble[1]. We believe this elevated level of extended concentration may begin to unwind in 2025 as investors recognize more attractive combinations of valuations+ earnings growth in the other non-Mag 7 stocks. We believe this “broadening” to other sectors and non-mega cap stocks is quite healthy for the overall global economy and long-term capital appreciation in equity markets.

Outlook

As mentioned earlier in this note, we believe we are on the cusp of a new economic cycle. As the cost of borrowing declines, we expect business and consumer credit activity to improve and capital spending to increase. We think companies have been destocking inventory levels since early 2023 to reduce exposure to weaker overall demand and profit margin risk. As a result, any improvement in end market demand should lead to an inventory restocking cycle. This would provide an additional tailwind to overall economic growth. Lower interest rates should also be a tailwind for long-duration assets like equities (i.e., lower discount rates). These factors should improve the economic outlook for the US economy in later 2025.

At Oliver Luxxe Assets, we focus on identifying businesses with strong ROIC, durable cash flow, and good reinvestment opportunities. Right now, we see many opportunities in the cyclical areas of the US economy with low valuations, strong cash flow, and low investor expectations. We believe this combination could lead to attractive returns over the coming years.

[1] a stock market bubble that ballooned during the late-1990s

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer:

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction. All investment strategies have the potential for profit or loss; changes in investment strategies may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the US market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to the success or lack of success of any particular investment strategy. All are subject to various factors, including, to general and local economic conditions, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.