As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Source: S&P Dow Jones Indices LLC

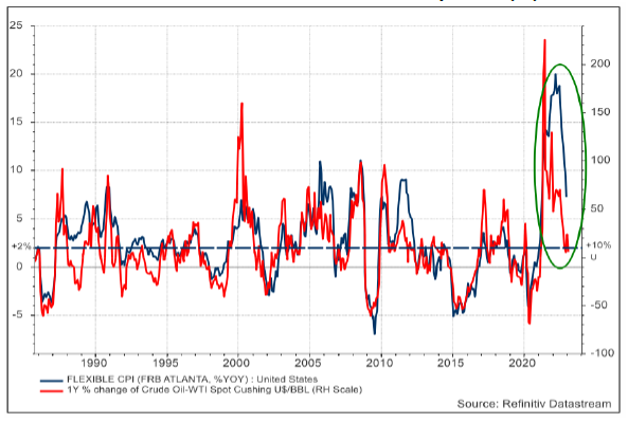

The Consumer Price Index (CPI) continued to move lower, reflecting a more normal balance of supply and demand across the basket of goods within the CPI index. CPI components such as new & used car prices and consumer electronic goods have shown some of the greatest normalization in prices. At the same time, shelter costs (i.e., rents and mortgages) and labor wages have remained at elevated levels and have proven to be “stickier.” Both wages and rents are negotiated infrequently, which is likely a key contributor toward the still elevated inflation.

Overall, we believe CPI will decline in 2023 from very elevated levels in 2022 as “flexible” CPI components subside. (See Chart below). However, we think the “sticky” components will remain persistently high. As a result, we believe Fed policy will remain restrictive through much of 2023 until the jobs market begins to slow to more acceptable levels.

The labor market in 2022 was very strong. For example, the US labor market reported a ratio of job openings to unemployed people of 1.7x (flat vs. 3Q22), which is well above the 2019 level of 1x [1]. This means that workers have leverage over employers (which is inflationary) and, in order to reduce this source of inflation, the Federal Reserve aspires to reduce job vacancies without meaningfully increasing the unemployment rate. High and increasing wages remain a bright spot when assessing an offset to a potential recession in the United States.

[1] Bureau of Labor Statistics

Equity Outlook

At Oliver Luxxe, we remain focused on identifying companies with strong balance sheets, attractive ROIC opportunities, and predictable free cash flow generation. We believe this will be increasingly important in 2023 due to the prospects for slower economic growth and higher cost of capital. We believe business models that fit this profile should be well-positioned to handle an economic downturn. Importantly, companies that possess these characteristics can opportunistically deploy excess capital in a shareholder-friendly manner (via M&A, buybacks, and dividends).

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer:

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “should,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including general and economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe Assets or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.”

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.