As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

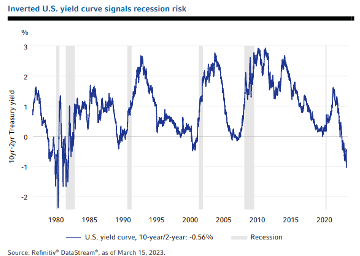

In March, the collapse of Silicon Valley Bank and Signature Bank represented the largest US bank failures since the global financial crisis in 2008. Concerns over the solvency of US regional banks stoked worries of financial instability, which led the US Federal Reserve to slow the rate of interest rate increases to 25 basis points (vs. 50 basis points prior). Markets are indicating that the banking system shock is expected to act as an additional form of restrictive monetary policy as institutions begin tightening their lending policies. Many investors believe that the interest rate hiking cycle is coming to an end, which led to outperformance in the technology sector during the first quarter. Recall that since March 2022, the US Federal Reserve has raised interest rates at the fastest pace since the 1980s, which has led to an inverted yield curve.

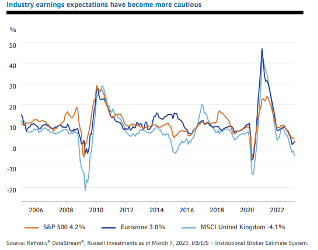

The US economy is sending mixed signals, as several leading indicators such as the US Manufacturing PMI are suggesting further deceleration. These datapoints are a result of monetary policy becoming less favorable in order to reduce inflation. We continue to believe that the cost of capital will remain higher due to slower, but resilient economic growth, along with gradually declining inflation. Several consumer price index (CPI) components, including energy and food, have fallen as supply and demand normalizes, but there are other components (wages and rents) that remain elevated. Wage inflation has spiked to 40-year highs due to an incredibly tight labor market where there are approximately two job openings for every unemployed person in the US.

Outlook

As we enter 2Q 2023, we believe the US economy will continue to slow, albeit at a subdued pace as employment levels and wages remain on solid grounds. Inflationary pressures are subsiding but should remain elevated due to a confluence of factors, including resilient consumer spending, reshoring of US manufacturing, and the Inflation Reduction Act generating another level of demand. As a result, we expect the cost of capital will remain high due to higher interest and tighter lending standards by financial institutions. Therefore, we believe balance sheet integrity, cash flow generation, and earnings stability remain critical elements to navigating a challenging macroeconomic environment. Despite this, any economic recession/slowdown should be shallow based on current data points.

On a more positive note, we expect the US economy to eventually enter another economic expansionary cycle soon. Simultaneously, we intensely focus on identifying attractively valued businesses trading at undemanding valuations. Recall, our investment process is focused on “Private Equity in the Public Marketplace.” The current uncertain macro environment and overall investor skepticism are presenting opportunities to identify high-quality businesses that are trading at a discount to their intrinsic value. We believe our clients’ portfolios should be rewarded over the next 3-5 years. Warren Buffet once said that it is wise for investors to be “fearful when others are greedy, and greedy when others are fearful”1.

[1] Berkshire Hathaway, Inc.

"Chairman's Letter, 1986

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer:

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “should,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including general and economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe Assets or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.”

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.