As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

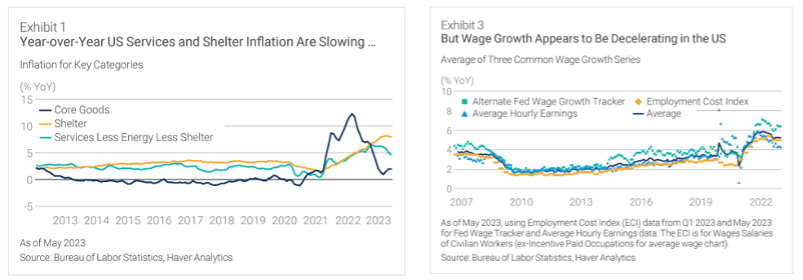

The rate of inflation continued to decelerate during the second quarter, as indicated by the Consumer Price Index (CPI) and Producer Price Index (PPI). The June Producer Price Index had a smaller-than-expected increase which could be the latest sign that inflation is headed in the right direction. The June PPI rose +0.1% for the month, which was below the consensus expectation of +0.2% and represented another month when inflation continued to decline. Core goods prices have rapidly declined in 2023, driven by upward surprises in overall supply chains and softening of consumer demand. Key areas of inflation such as housing/rents, autos, and services prices have started to roll-over, potentially setting up the likelihood of continued disinflation.

The US economy is sending mixed signals, as several leading indicators such as the US Manufacturing PMI are suggesting further deceleration. These datapoints are a result of monetary policy becoming less favorable in order to reduce inflation. We continue to believe that the cost of capital will remain higher due to slower, but resilient economic growth, along with gradually declining inflation. Several consumer price index (CPI) components, including energy and food, have fallen as supply and demand normalizes, but there are other components (wages and rents) that remain elevated. Wage inflation has spiked to 40-year highs due to an incredibly tight labor market where there are approximately two job openings for every unemployed person in the US.

2Q 2023 Outlook

A few decades of equity investing, especially in the Small and Midcap arena, has taught us many lessons. One such lesson is macro-related uncertainty and overall investor anxiety oftentimes creates valuation dislocations leading to attractive long-term opportunities, just as it did in 2000 after the Internet Bubble and early 2009 after the Great Financial Crisis.

At Oliver Luxxe, we use a “Private Equity in the Public Marketplace” approach towards equity investing. Our process does not require us to formulate top-down macro or interest rate forecasting. Instead, we focus our time and efforts conducting in-depth fundamental valuation analysis especially during times of investor angst and uncertainty. We also seek to target companies that are levered toward secular growth themes, which can provide revenue and earnings growth during periods of softer economic growth. For example, key areas of secular growth are re-shoring of supply chains, the Inflation Reduction Act (IRA) spending, and Artificial Intelligence applications. Additionally, cyclical areas such as semiconductors, trucking and housing-related industries have attractive risk/reward potential over the next 3–5-year periods. In summary, we are finding attractive investment opportunities especially within the small/midcap arena where valuation spreads are the widest since the aftermath of the Internet Bubble in 2000.

NOW IS NOT THE TIME TO BE FEARFUL!

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer:

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “should,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including general and economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe Assets or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. All investment strategies have the potential for profit or loss and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio.