As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

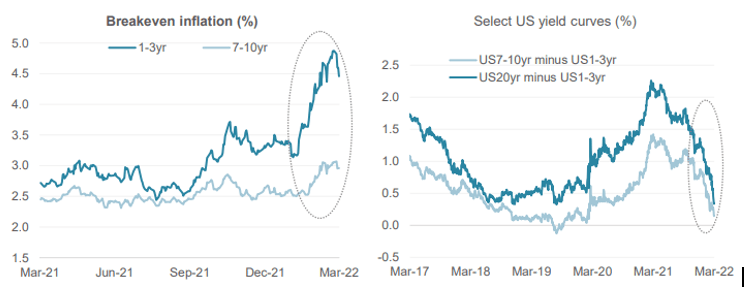

During the first quarter of 2020, governments worldwide implemented aggressive monetary and fiscal policies to fight the initial COVID lockdown. These actions effectively increased aggregate consumer demand, which tends to be inflationary. Importantly, as the global economy exited COVID in 2021, many of the bottlenecks in the global supply, including semiconductor shortages and logistical bottlenecks, further exacerbated the demand/supply imbalance, resulting in even higher prices for goods and services.

As we enter 2H 2022, many supply chain constraints/bottlenecks are easing, including lower freight costs, housing prices, and commodity prices (lumber, metals, and energy). We believe tighter monetary policy is starting to slow down a “red-hot” US economy. As a result, we expect the overall inflation level will remain elevated above the Fed’s 2% long-term target rate, but the nominal inflation level may have already peaked. In fact, the Citi global supply chain pressure index for June 2022 showed a meaningful easing of global supply-chain conditions (see figures 13 & 14 below).

The equity market is a forward-looking discounting mechanism, so any decline in the overall rate of change in inflation should be viewed positively by market participants.

OUTLOOK:

As we previously noted, most of the equity market's decline this year has been driven by price/earnings multiple compression. We still believe that consensus earnings for 2H2022 and 2023 need to be revised downwards. In the current environment, focusing on companies' balance sheets and cash flows is paramount as the cost of capital is increasing while earnings and profit margins are under pressure, driven by higher input costs and slowing demand. We remind readers that the "bottoming" of the overall equity market is a process, not an event.

We continue to prioritize companies with low debt levels, limited variable rate debt financing, attractive valuation multiples, and experienced management teams. During times of market volatility and economic turbulence, shares of high-quality businesses are often available at undemanding valuations. At Oliver Luxxe, our quantitative and fundamental process provides us with a disciplined framework to identify and select these types of businesses. We believe our investors/clients will be rewarded over the next 3-5 years.

[1] Goldman Sachs

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer: This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “should,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including general and economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe Assets or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.